Experts say repeated hurricanes are leaving financial devastation long after the winds die down.

Florida’s hurricane seasons are bringing more than wind and rain — they’re bringing financial ruin for thousands of homeowners. As powerful storms grow stronger and more frequent, insurance premiums are skyrocketing, repair costs are soaring, and many residents can’t keep up. When disaster strikes twice or even three times in a few years, the bills pile up faster than relief funds arrive. Economists warn that the state’s foreclosure rates are rising, revealing the hidden economic toll of climate-driven storms.

1. Storm damage often leads to costly repairs that burden homeowners financially.

Storm damage often inflicts costly repairs that place a heavy burden on homeowners. When roofs leak and windows shatter, repair costs can quickly add up. These expenses can destabilize family finances, leading some owners to fall behind on their mortgage payments and face possible foreclosure.

For families already stretched thin, unexpected repair costs can prove daunting. If insurance coverage falls short or is delayed, homeowners may use savings earmarked for mortgage payments, heightening financial distress. Persistent financial strain from repairs can make staying on top of mortgage obligations challenging, increasing foreclosure risks.

2. Flooding can cause extensive property damage, reducing home value significantly.

Flooding leaves a trail of property damage that can severely impact home values. Waterlogged floors, ruined drywall, and mold infestations are common issues, often reducing the desirability and market value of affected homes.

With lower property values, selling or refinancing becomes difficult, trapping homeowners in homes worth less than their mortgages. Prospective buyers often shy away from flood-damaged properties due to potential future risks. This cycle can exacerbate financial pressure on homeowners, pushing some toward foreclosure.

3. Insurance claims may be delayed or denied following severe weather events.

Insurance claims don’t always materialize swiftly after severe weather events, delaying critical repairs. In some cases, policyholders face denied claims due to policy loopholes, leaving them with unexpected costs.

The uncertainty of insurance payouts leaves homeowners in limbo. Extended delays can exacerbate existing damages, further depreciating property value and complicating financial recovery. This waiting game adds to homeowners’ stress and financial burdens, potentially leading to increased foreclosure risks.

4. Repeated storms increase maintenance expenses, making mortgages harder to manage.

Maintenance expenses rise with repeated storms. Each event can erode property integrity, necessitating ongoing repairs. When new storms hit, older damage compounds, creating a never-ending cycle of upkeep costs.

Homeowners face mounting financial strain juggling recurring repairs and mortgage obligations. Repeated outlays can erode savings faster than anticipated, leaving little room for unexpected expenses. This scenario can make mortgage management increasingly challenging, increasing the likelihood of defaults and foreclosure.

5. Damaged infrastructure can impact community services and local property attractiveness.

Damaged infrastructure following storms can disrupt community services, affecting local property value. Downed power lines, impassable roads, and compromised water supply can make areas less appealing.

As infrastructure struggles, local properties may lose attractiveness to potential buyers. This broader community disruption can slow post-storm recovery. Property values can stagnate or drop, making it difficult for homeowners to refinance or sell, thereby escalating financial strain.

6. Temporary displacement reduces income stability and disrupts mortgage payments.

Temporary displacement impacts income stability, disrupting mortgage payments. Families forced to vacate their homes might face unexpected accommodation and travel costs.

The financial burden of temporary housing and a disrupted routine can exacerbate financial pressure. Without steady income, staying current on mortgage payments becomes tougher. This instability may lead some to seek forbearance or fall behind, increasing foreclosure risks.

7. Lenders may reassess property risk, tightening loan conditions for storm-prone areas.

Lenders may reassess the risk profile of storm-prone properties, tightening loan conditions. Enhanced safety measures or higher insurance requirements could become prerequisites. This approach can reflect lenders’ concerns about future neighborhood viability.

Stringent loan conditions can deter potential buyers and complicate refinancing efforts. Homeowners facing refinancing hurdles or higher costs may struggle to maintain financial stability. Such conditions can raise the stakes, possibly tipping more homeowners toward foreclosure.

8. Property tax hikes sometimes follow disaster recovery efforts, adding financial pressure.

In the wake of a disaster, rising property taxes can add financial strain as municipalities seek recovery funds. Homeowners already stretched by repair costs and insurance hassles might find tax hikes unbearable.

Higher taxes intensify financial pressure, making mortgage payments harder to manage. Families may have less disposable income for other necessities, heightening financial vulnerability. The added burden can push some over the brink, leading to increased foreclosure incidences.

9. Declining neighborhood appeal after storms can slow property sales and refinancing options.

After severe storms, declining neighborhood appeal can stifle property sales and refinancing opportunities. When fallen trees and debris linger, the neighborhood’s draw diminishes.

Prospective buyers might shy away from areas appearing neglected or frequently disrupted by storms. Homeowners might face stagnant property values and refinancing challenges, trapping them in unfavorable financial situations. Slow sales and refinancing can exacerbate economic stress, contributing to foreclosure risks.

10. Limited availability of skilled contractors can extend repair timelines and costs.

A shortage of skilled contractors post-storm can delay necessary repairs, driving up costs. When demand outstrips supply, repair timelines extend, postponing homes’ return to market-ready conditions.

Extended timelines can escalate damage and diminish property values further. The wait and higher costs can strain homeowners already contending with stretched finances. This prolonged recovery can make regular mortgage payments difficult, risking increased foreclosure scenarios.

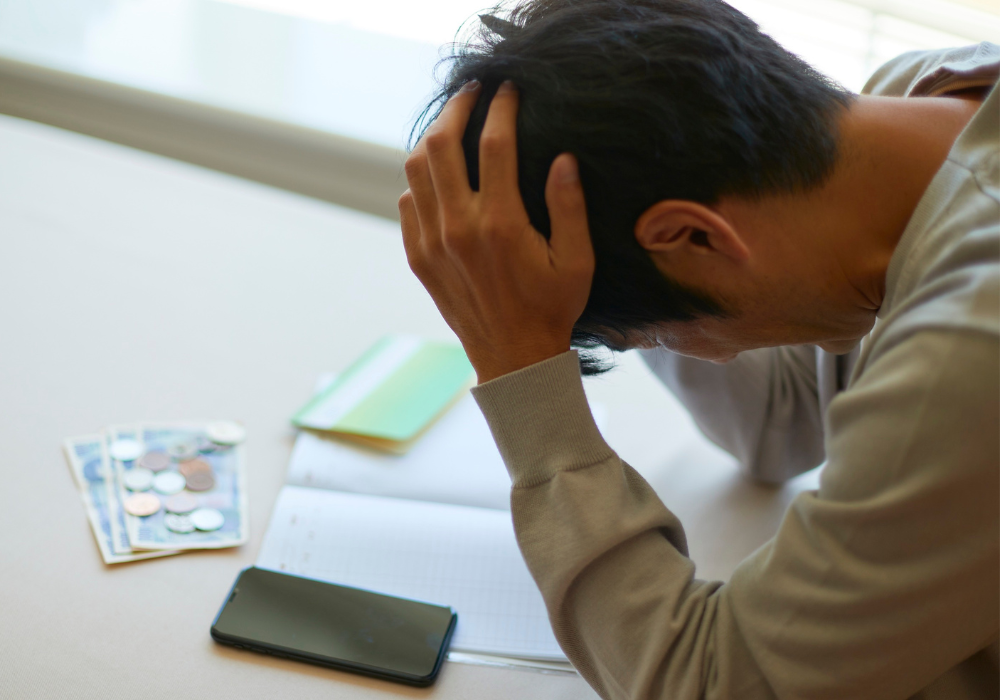

11. Emotional stress from storm impacts can affect homeowners’ financial decision-making.

Emotional stress from storm impacts can influence homeowners’ financial decisions, affecting judgment. When anxiety clouds discernment, financial priorities may shift.

The psychological toll can lead to overlooked payments or ill-considered financial choices. Persistent stress from unpredictability might erode savings or derail budget plans. These mental burdens can exacerbate economic challenges, increasing the likelihood of foreclosure.